Direct Payment Types | Setting Up Direct Deposit | Example Scenarios

EBMS can be used to process electronic direct payments to employees and vendors and to receive electronic payments from customers. The following technology is used to process these direct payments:

-

United States: Automatic Clearing House (ACH) is used primarily for business to business (B2B) and payroll.

-

Canada: Electronic Fund Transfer (EFT) is the backbone of the Canadian payment industry including debit and fund transfers. Contact Eagle Software Canada for assistance to configure EFT transactions.

Video: Direct Payments ERP Support Training

EBMS implements direct payments in the following processes:

-

Direct Deposit Payroll: Review Direct Deposit Overview for instructions to electronically pay workers for labor.

-

Direct Vendor Payments: Review Direct Vendor Payments ACH for more information on sending electronic payments directly to vendors.

-

Receive Direct Payments from Customers: Review ACH Customer Payments for details to collect accounts receivable payments electronically from customers.

The user must establish online banking services with any banks that will process an ACH Transaction file before the direct payments option can be put into operation. Speak to a customer service representative at your bank who specializes in corporate or business online services to determine whether direct deposit capabilities are available. Direct deposit transactions must be approved by the bank before implementing the service within EBMS.

There will be enrollment forms to complete and return to the bank so they can set up online banking access for your company. The bank’s approval time in implementing direct deposits must be considered while planning on setting up and using this feature within EBMS. Make sure to budget in enough time for communication with the bank before implementing ACH.

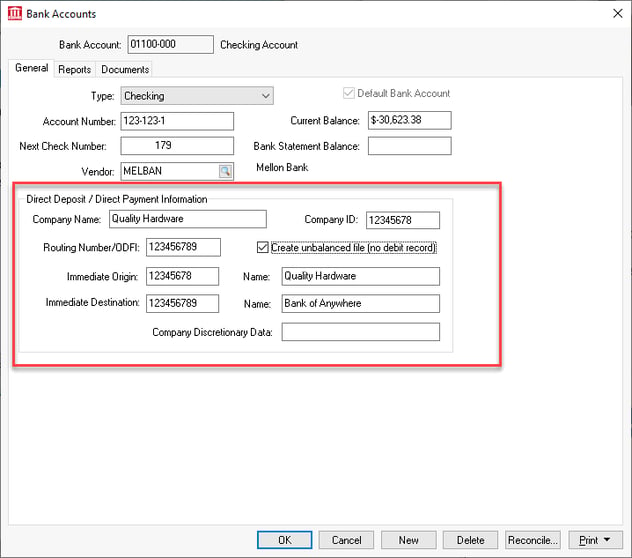

Set Up EBMS Bank Accounts for ACH

Complete the following steps to configure the bank account information within EBMS:

Enter the bank’s routing information for each company bank account used to transfer direct deposit transactions. This account is normally the checking account used for payroll.

Go to and select the bank account used to make or receive direct payments. Look at the General tab of the bank account record to configure settings for Direct Deposit / Direct Payment Information:

-

The bank account Type should be set to Checking.

-

Enter or verify the bank account number within the Account Number entry. As the source of funds for the direct deposit transactions, this should be the company’s payroll bank account number within the originating bank. The bank account number is part of the line of numbers printed along the bottom of pre-printed checks and pre-printed deposit slips. Look for the second set of numbers in that line. The account number should also be the longest set of numbers.

-

Enter the Account Number, Next Check Number, Vender Setting, etc. Review Changing Bank Account Information for more details on these settings.

-

Enter the Company Name as required by the bank that will be processing the direct payments. The Company Name may need to appear in the exact syntax that the bank requires, so check the bank requirements first. Because of a limit on the number of characters in this field, the bank may require an abbreviated copy of the company name.

-

Enter the direct payment Company ID, which is the identification code for the employer or sender. This exact employer identification code is defined by the bank and must be formatted properly with dashes. The bank may ask the company to use its tax identification number or EIN number. Copy the Company ID and Company Name directly from the direct deposit agreement from your bank or consult with your bank to get these exact values.

-

Enter the Routing Number of the originating bank in the Routing Number/ODFI field. As the origin of funds for the direct deposit transactions, this should be the bank’s unique identifying number within the Federal Reserve System. The routing number is part of the line of numbers that is printed along the bottom of pre-printed checks and pre-printed deposit slips. It typically 9 digits long and the first set of numbers on the left-hand side.

-

Enable the Create unbalanced file (no debit record) option only if required by the destination bank.

-

Enter the Immediate Origin code. This setting is an ACH origin or sending point identification number.

-

Enter the ACH origin or sending point Immediate Origin Name. This is usually the EBMS company name.

-

Enter the Immediate Destination code. This is the receiving point or ACH Identification number of the destination bank.

-

Enter the Immediate Destination Name. This is the ACH destination or receiving point name. This is usually the destination bank name. It is recommended that the user consult with the bank to determine if there is a standard bank name that should be utilized for this entry.

-

Enter the optional Company Discretionary Data only if required by the bank. This value will be placed in the batch header record starting in column 4. This information consists of exactly 20 numeric characters. Most banks do not require this code.

-

Review Create Prenote and Submit NACHA to Bank Web Portal for steps to test bank information.

Review Reconciling a Bank Account for steps to review and reconcile ACH payment transactions.

Example Scenarios:

Scenario 1: An equipment sales and repair company processes payroll using the EBMS labor module. The payroll includes hourly pay for service technicians, commission pay for sales staff, and salaried pay for managers. Most of this payroll is paid to employees using the direct deposit payment method instead of printing pay checks. The sales managers' pay is deposited into two bank accounts based on a predetermined ratio. A NACHA file is created by EBMS containing the pay for all employees. This file is uploaded weekly using the ACH or EFT tools within the company bank’s online cash management portal.

Scenario 2: A small manufacturer purchases most of their raw materials from a single supplier. This company subcontracts some of the manufacturing processes to sub-shops that requires regular payment transfers. This company pays vendors using a direct electronic payment rather than using printed checks or a more expensive credit card payment. This systematic direct payment process, in conjunction with the AutoSend document email tools, requires a limited amount of clerical effort. This timely method of paying partners reduces postage and specialty forms.

Scenario 3: A plumbing and HVAC contractor offers preventive maintenance contracts for various of their client’s heating and air conditioning units. Billing clients monthly is the preferred payment method for both the contractor and their clients. Processing costs are reduced substantially by using the new EBMS direct payment feature instead of credit cards. The credit card fees are not part of the direct payment amount, which allows the contractor to reduce costs and offer a more economical contract. The contractor processes these contracts on a weekly basis based on the contract date. Each batch of contracts is compiled into a NACHA file and uploaded to their bank, which processes the transfer of funds.